on Sektkellerei Schloss Wachenheim AG (ETR:SWA)

Schloss Wachenheim AG: Positive Outlook with Increased Price Target

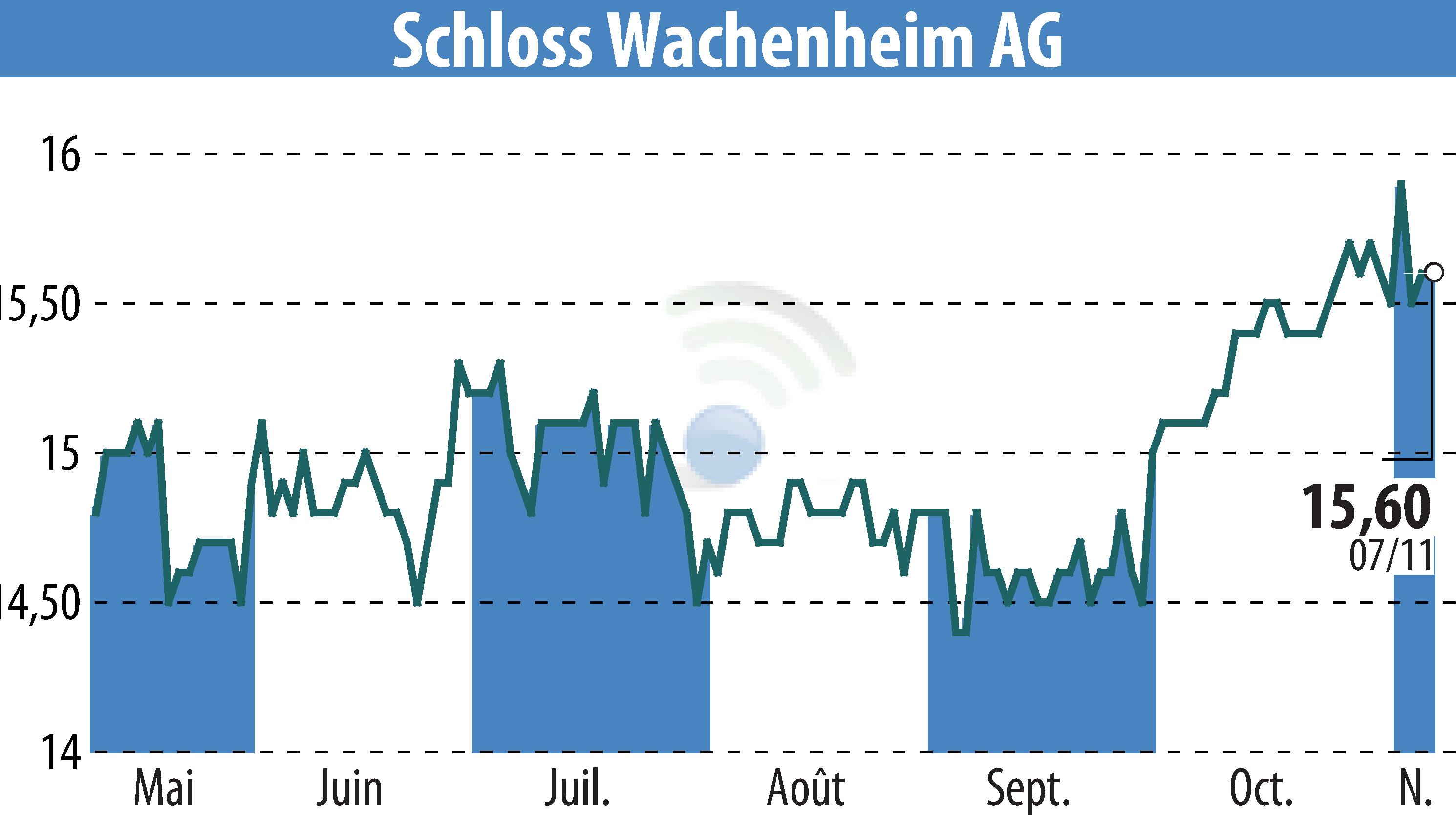

First Berlin Equity Research has released an update on Schloss Wachenheim AG, confirming a 'Buy' recommendation and adjusting the price target from €19 to €20. The change reflects improved forecasts and a decline in the 10-year German bond yield to 2.66% from 2.75% since late September. The company's Q1 2025/26 bottle sales rose by 6.7% to 54.9 million, marking the largest quarterly increase in over five years, driven by a robust private label sparkling business in Germany and recovery in the French market.

Sales growth, however, was lower than volume growth at 3.5%, totaling €106.0 million, influenced mainly by product mix effects. EBIT exceeded expectations, reaching €5.3 million, driven by the improved profitability of the France segment. The management remains optimistic about the Christmas quarter and maintains guidance for full-year EBIT between €30 million and €33 million, with profit before non-controlling interests forecasted at €18 million to €21 million.

R. E.

Copyright © 2026 FinanzWire, all reproduction and representation rights reserved.

Disclaimer: although drawn from the best sources, the information and analyzes disseminated by FinanzWire are provided for informational purposes only and in no way constitute an incentive to take a position on the financial markets.

Click here to consult the press release on which this article is based

See all Sektkellerei Schloss Wachenheim AG news